On June 2, satellite imagery derived analytics provider RS Metrics hosted a webinar discussing the recent trends in the commodities metal market.

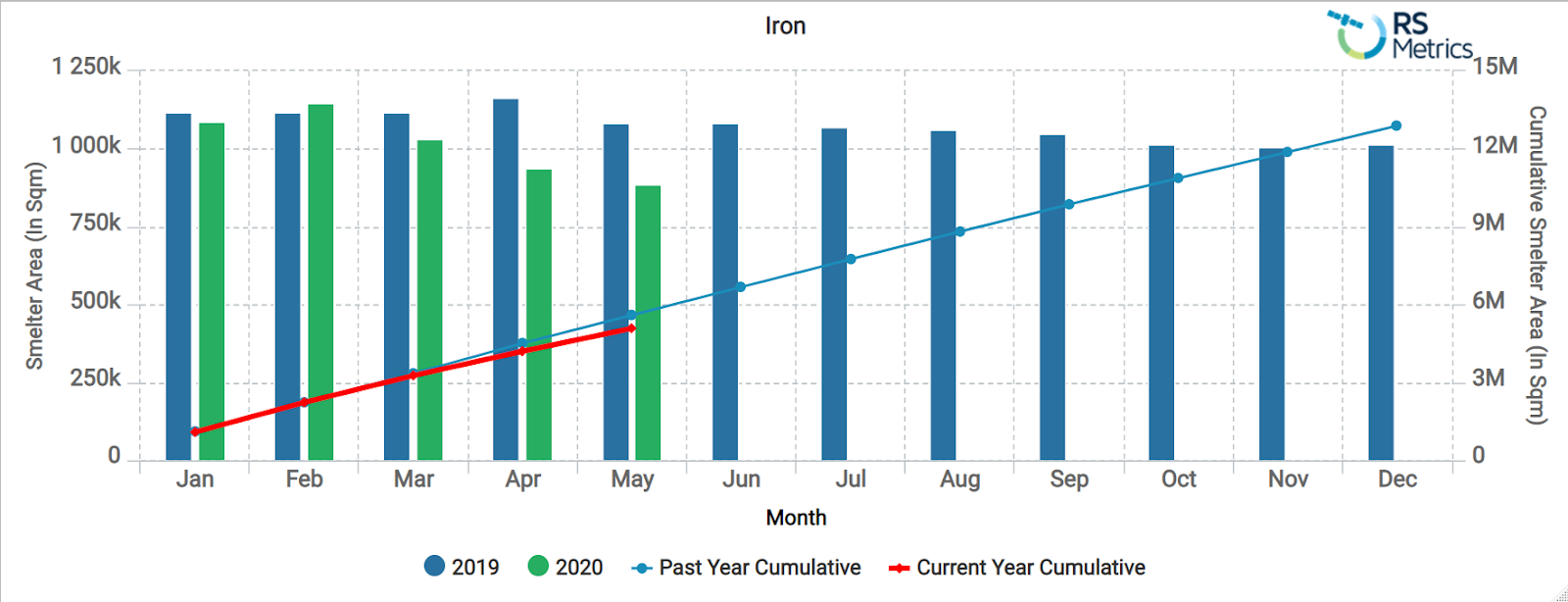

MetalSignals™ is one of RS Metrics’s main products, as it monitors and analyzes Aluminum, Copper, Zinc, and Iron Ore at approximately 500 smelters and storage sites globally. The product covers metal and concentrate stockpiles, finished products (ingots, cathodes, etc.), copper anodes, semi-trailer trucks, employee cars, and dump trucks and tippers to gauge a certain location’s production. MetalSignals™ also uses SAR(Synthetic Aperture Radar) in addition to optimal imagery as it allows monitoring through clouds, which is advantageous for measuring Iron Ore specifically.

MetalSignals™ is extremely useful at explaining recent trends in the metals’ markets, as it provides inventory statistics which can give supply side context to market events.

Iron Ore has experienced recent price strength, as its benchmark 62% contract prices have rallied 14% in the past month, rising above $90/ton for the first time since July last year.

There are several key reasons for this price strength, including China’s 5.8% increase in imports during Jan-April 2020 compared to that same period a year prior, China’s increasing steel production contrasted with decreasing global iron ore production, Iron Ore supply side disruptions, strong rebar demand for construction activity, decreasing iron ore port inventories in China and Brazilian production weakness due to the impacts of COVID-19.

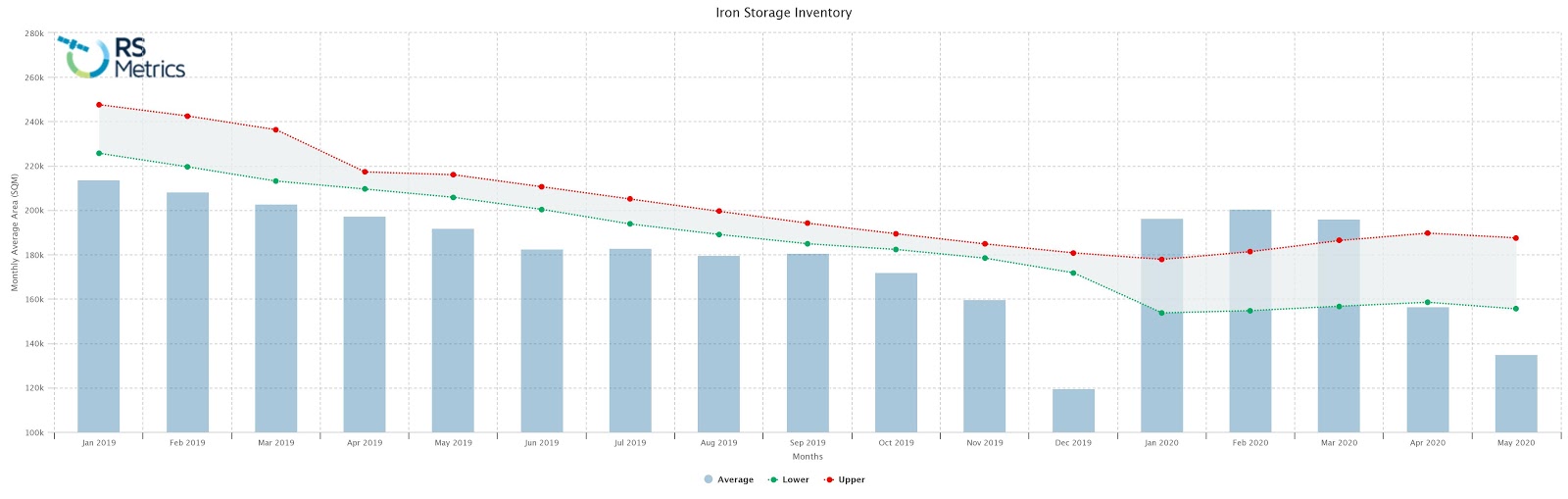

RS Metrics China Iron ore Port Inventory:

Brazilian exports, which were rising prior to the effects of COVID-19 taking hold, have dropped, contributing to a drop in the Baltic Dry Index which was recovering from a poor Q1 due to weather related disruptions.

Ponta Da Madeira Port Inventory (Brazil):

Base Metals Update:

The recent events in the markets for the other three base metals can be characterized by three key trends:

- Decreasing inventories in China

- Significant global production disruptions due to shutdowns

- Traders were positioned short in Q1-2020 but decreasing inventories and production shutdowns provided price support

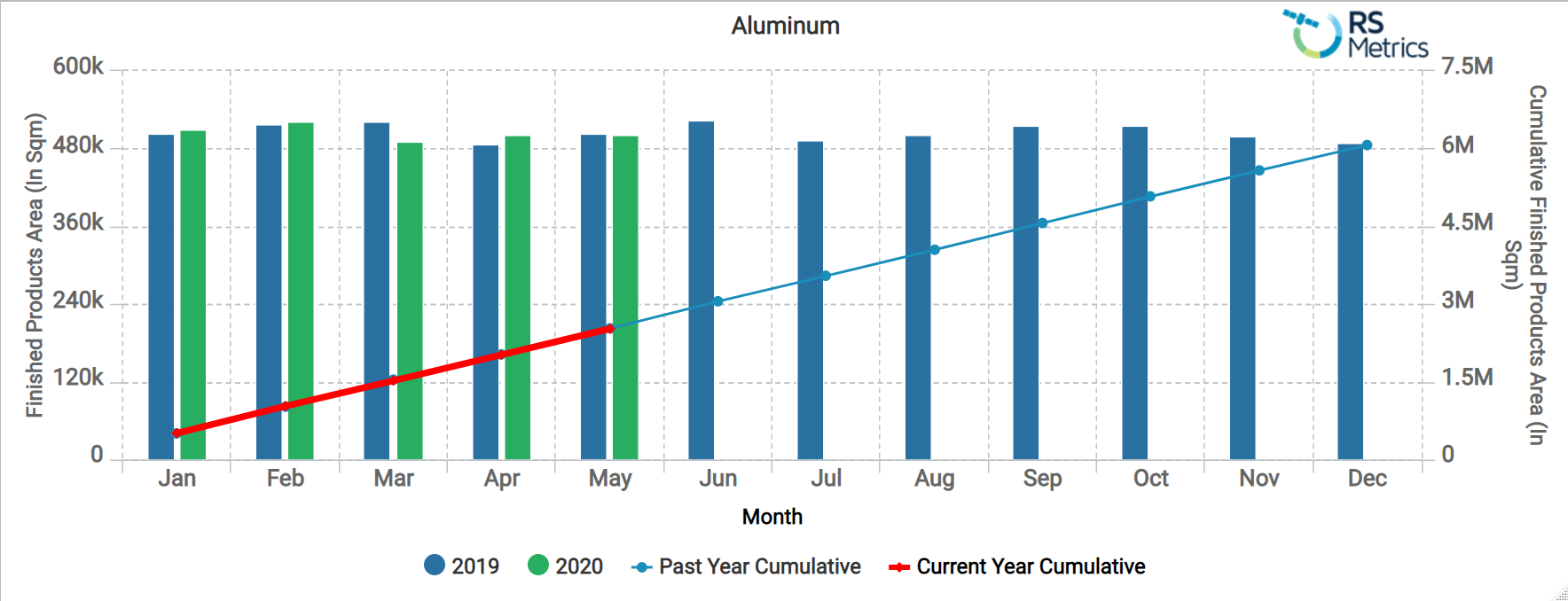

Aluminum: The Aluminum market has, thus far, been relatively unscathed by shutdowns, as only 4-5% of the total capacity is currently suspended. Global Aluminum production for Jan-April 2020 increased by 1.5%, with the bulk of it coming from China, where smelters increased their output by 2.2% despite quarantine measures and a collapse in demand from product manufacturers.

RS Metrics Aluminum Smelter Inventory Trends:

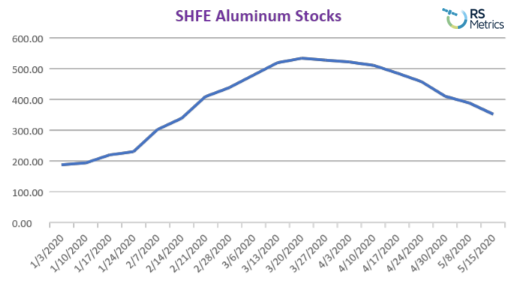

The decreases in Chinese smelter inventory tracked by RS Metrics from March-May 2020, shown below, depict increasing demand in Q2-2020, are reflected in corresponding shifts in SHFE Aluminum stocks as well.

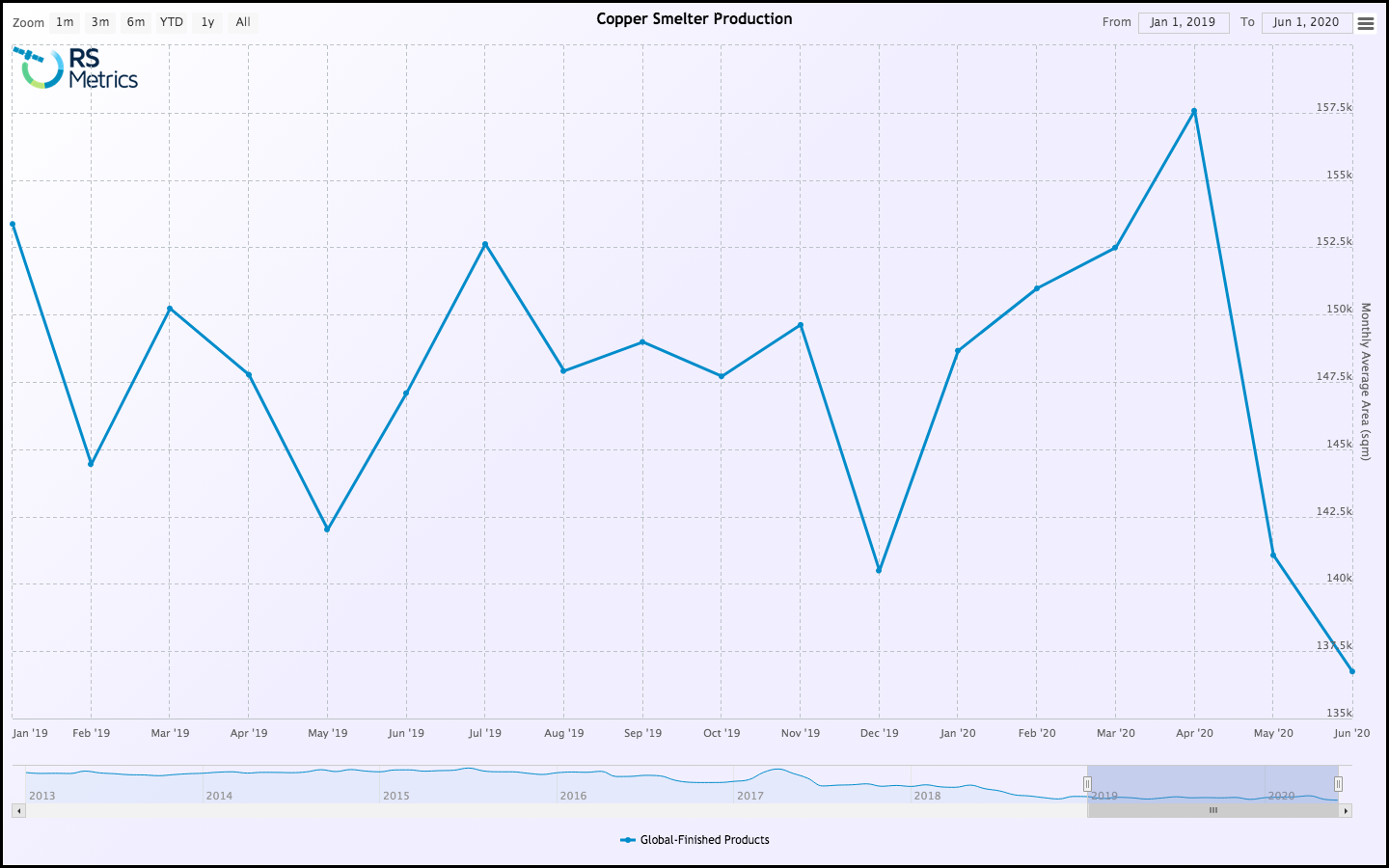

Copper: Despite 12% of Copper mine supply being suspended, Copper’s price has rallied, recovering from the 4 year low of $4400/ton in March 2020 and now trading at over $5700/ton. This recent price strength is also due to China’s recovery and supply cuts underpinning the market. The official purchasing manager’s index has increased from its low in February and remained in expansionary territory in May.

RS Metrics Copper Smelter Inventory Trends:

The increasing Chinese demand is reflected in the decreasing smelter & warehouse inventories. The smelter inventories tracked by RS Metrics are a leading indicator of the changes in warehouse inventories and ultimately SHFE & LME price changes.

MetalSignals™ is also an extremely advantageous tool for predicting price levels. As explained in the webinar, MetalSignals™ allows one to have an independent third-party observation of on the ground inventory, lessening reliance on anecdotal evidence. It provides traders and risk takers with reliable data points, helping to paint an accurate picture of the state of the market.

The July COMEX Copper contract rose 25% from its low on March 19, while LME Copper rose 15.48% from its low on March 23. Copper is known to reflect broader economic action, and this was illustrated by FCX, an oft traded proxy for copper that hit a low on March 18 at $5.31, but closed May 29 at $9.11, rising 39%, the same percent increase as the SPY index.

As Senior Adviser Peter Neumann wrote, “the price trends that RSM presented in our webinar of June 2 remain intact.

LME exchange inventories continue to decline from their recent peak in March 2020, and RSM's observation data indicates a continuation of global inventory reduction. This generally soft supply picture could be expected to underpin copper prices in the near term and should support the rising prices. Observed near term support/ resistance prices are seen as $5500/mt and $6000/mt. There are "re-opening' steps being taken slowly and unevenly around the world by governing bodies. As these changes take hold in whatever magnitude, it will be important now to closely monitor the beginnings of directional shifts in inventory as they could be the seeds for continuation patterns."